Ricky Cheng, Director and Head of Risk Advisory, BDO Risk Advisory Services Ltd, looks at the roles company secretaries can play in climate governance and in implementing the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD).

In August 2021, the Intergovernmental Panel on Climate Change (IPCC) issued the first working group report of its Sixth Assessment Report – Climate Change 2021: The Physical Science Basis. According to the report, human-induced climate change is already affecting many weather and climate extremes in every region across the globe. Global warming of 1.5°C and 2°C will be exceeded during the 21st century unless deep reductions in carbon dioxide and other greenhouse gas (GHG) emissions occur in the coming decades. Before the situation gets worse, companies should implement the TCFD recommendations to provide climate-related information to their stakeholders on how they address the impacts arising from climate change and its related risks and opportunities.

An introduction to the TCFD recommendations

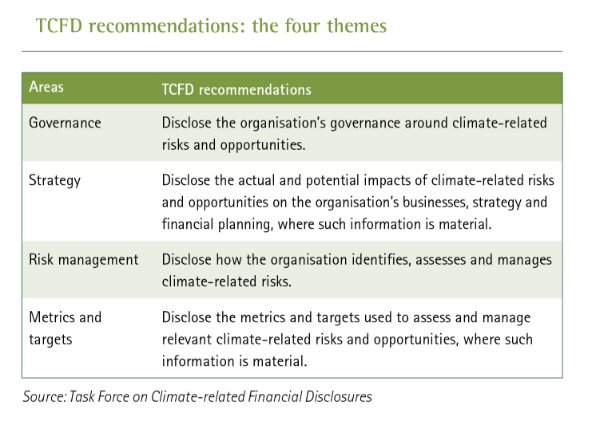

The Financial Stability Board created the TCFD to improve and increase reporting of climate-related financial information to stakeholders. In 2017, the TCFD issued a report which made 11 disclosure recommendations around four thematic areas (see 'TCFD recommendations: the four themes'). The report explained that climate-related risks and opportunities should be integrated into companies' strategic planning and enterprise risk management (ERM) frameworks, assessing their impacts on a company's operations under different time horizons and then disclosing the related financial impacts. The report also illustrated the potential financial impacts of climate-related risks, namely physical and transition.

As the risks of global warming become ever clearer, regulators are making climate risk disclosure mandatory at a faster pace. In the US, the Securities and Exchange Commission is expected to propose a series of new climate risk disclosure requirements for companies by the end of 2021. In Japan, companies listed on the Tokyo Stock Exchange 'Prime' market will be required to comply with mandatory climate risk disclosure requirements aligned with the TCFD recommendations from April 2022. In Hong Kong, the Securities and Futures Commission will require fund managers to manage and disclose their climate-related risks with reference to the TCFD recommendations with effect from August 2022 for large fund managers and November 2022 for other fund managers. Hong Kong listed companies are also required, on a comply or explain basis, to disclose significant climate-related issues in accordance with the latest ESG Reporting Guide issued by Hong Kong Exchanges and Clearing Ltd. In December 2020, the Green and Sustainable Finance Cross-Agency Steering Group announced plans to make TCFD-aligned disclosures mandatory across all relevant sectors no later than 2025.

In addition to the tougher regulatory approach, companies are also subject to increasing stakeholder pressure for voluntary TCFD-aligned disclosures. In 2021, BlackRock Chief Executive Larry Fink’s letter to chief executive officers mentioned that climate change is already causing companies to write down stranded assets and, at the same time, increasing their focus on the significant economic opportunities that the transition will create.

Companies are also increasingly exposed to climate-change related litigation from various stakeholders. According to the Climate Change Litigation Update, August 2021, by Norton Rose Fulbright, the total number of climate change cases filed as at July 2021 had reached over 1,800 globally. In May 2021, a Dutch-based global oil company was ordered by the court to reduce its carbon emissions to 45% by 2030, compared with 2019 levels.

Companies are also increasingly aware of the benefits of implementing the TCFD recommendations. These may include:

- easier or better access to capital by increasing investors' and lenders' confidence that the company's climate-related risks are appropriately assessed and managed

- increased awareness and understanding of climate-related risks and opportunities within the company, resulting in better risk management and more informed strategic planning, and

- proactively addressing investors' demand for climate-related information in a framework that investors are increasingly asking for.

According to the TCFD 2021 Status Report (issued in October 2021), there are over 2,600 companies worldwide (representing a 73% increase compared with 2020) supporting the disclosure of TCFD recommendations. Some of the key findings of the status report include:

- the process of estimating financial impacts can lead to improved internal and external communication

- allocating sufficient resources to assessing financial impacts helps timely development of decision-useful information, and

- rating agencies regard climate-related information as an increasingly important input in their financial impact assessments, informing the rating process.

How can the company secretary help?

The board has a fiduciary duty and accountability for the company's long-term sustainability and resilience with respect to potential changes in the business model that may result from climate change. Board meeting time is valuable, but climate change has to be on the board's agenda from a compliance standpoint as a result of the disclosure requirements stipulated in the ESG Reporting Guide. Given the governance role of company secretaries, they are critically positioned to advise boards on the significance of the potential impacts that climate change may have on business operations. They can also ensure discussion among board members of key climate-related issues, and promote a proactive effort by the board to address stakeholders' increasing need for climate-related disclosure information by implementing the TCFD recommendations.

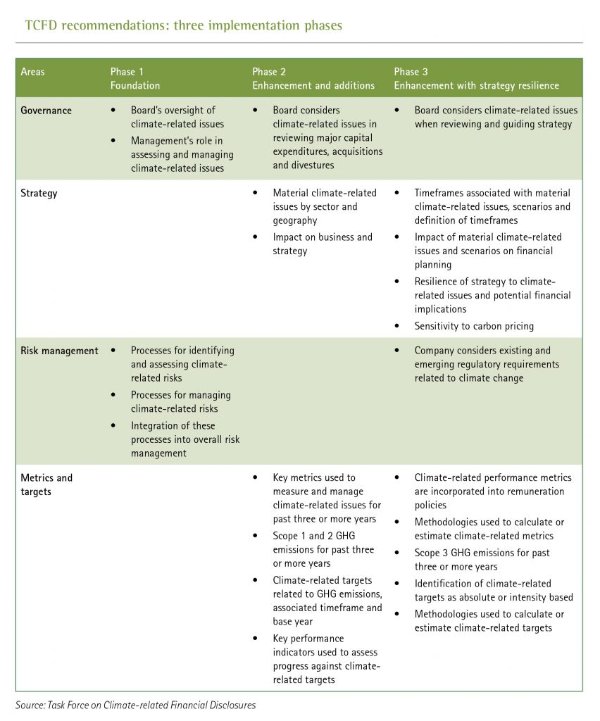

Depending on the impact of climate change issues on the company's operations, the level of its commitment and the maturity of its climate change management, company secretaries may assist the implementation by phases as recommended in the TCFD Status Report 2020 (see 'TCFD recommendations: three implementation phases').

Five key ways that company secretaries can assist in climate governance and help implement the TCFD recommendations are explored below.

1. The company secretary as climate governance professional

Company secretaries can assist organisations in building their climate governance infrastructures, including putting in place structures, policies and procedures for managing climate-related risks and opportunities. They can also help by improving the boards' and management's understanding of their roles and responsibilities in creating a good culture for effective climate governance. Some practical ways in which company secretaries can assist with climate governance are:

- ensure climate-change related oversight roles and responsibilities are incorporated in board and subcommittees' mandates

- advise the board to set up a dedicated subcommittee to manage climate change issues if their impacts are financially material to the company

- ensure climate-change elements are embedded in the board and corporate culture and values

- ensure the board is well informed of the latest climate-related trends through continuous training

- help the board understand how management identifies, assesses and manages climate-related risks and opportunities

- assist in capacity building by advising the board and the nomination committee to consider including climate-related expertise in their composition, and

- ensure that management takes up its role in assessing and managing climate-related issues.

2. The company secretary role in strategy

The uncertain and dynamic nature of climate change may affect the long-term viability of a company. It is therefore crucial that the board regularly assesses the resilience of the company's strategy and operations with regard to climate change under different scenarios and related mitigating measures. Company secretaries should ensure that there are adequate strategic discussions on climate change issues at board meetings. These meetings should cover, but not be limited to, the following:

- trends in sustainability or decarbonisation practices in the industry

- the type of climate-related risks and opportunities that the company is facing

- the potential financial impact and priority of these material risks and opportunities on business strategy, model, operations, sectors and geography

- the estimation of when these material climate-related financial impacts may materialise

- resilience of the company's strategy regarding climate change under different climate scenarios, and

- regular updates on scenario analysis and related assumptions by management.

Company secretaries should also ensure that the discussions are in line with the company's long-term strategic goals and objectives, and in the best interests of the company. If the discussion results in significant business decisions being made, such as making changes to the business model or closing or acquiring business units in response to climate change, the company secretary should facilitate the board's engagement with shareholders on the proposed changes. The company secretary should also ensure that the strategic planning and decisions made by the board are well documented for future reference.

3. The company secretary's role in risk management

Climate change will give rise to a set of new risk factors, including both physical and transition risks, affecting the company’s operations. The board must take a leadership role in the management and oversight of climate-related risks and opportunities. Traditionally, the audit committee has been assigned with the responsibility for oversight of risk management and internal controls. In the context of climate change, the audit committee's role may include:

- initiating the identification of financial risks that arise as a result of physical and transition risks, which will facilitate comprehensive valuation of financial risk

- incorporating a climate change lens across the three lines of defense: business ownership, risk management and oversight of internal audits, and

- validating and incorporating climate-related financial disclosures within the remit of corporate disclosure.

Company secretaries have a responsibility to assist both the board and the audit committee in meeting their responsibilities by:

- ensuring climate-related risks and opportunities are on the board agendas

- advising the board on policy and legal risks such as possible tightening of rules and regulations concerning energy-efficient standards, the introduction of carbon tax and possible litigation brought about by stakeholders

- ensuring the board understands that there are robust risk management processes and procedures for managing climate-related risks

- ensuring that management integrates climate risks into the company's ERM framework to identify, assess and mitigate

related risks - ensuring that the roles of the audit committee mentioned above are incorporated in its mandates

- ensuring the audit committee understands the methodologies and policies used to develop the metrics, as well as the internal controls in place to ensure accuracy, reliability and consistency of the metrics period over period

- ensuring the audit committee assesses the relevance and impact of climate-related risks on financial statements, and the quality and accuracy of climate-related financial disclosures

- ensuring that the external auditor is engaged to evaluate audit quality of climate-related risk and performance disclosures and the likelihood of the external auditor raising climate-related risks as a 'key audit matter', and

- coordinating management and internal auditors in assessing the effectiveness of risk management measures on material climate-related issues and communicate the findings to the audit committee and the board.

4. The company secretary's role in monitoring risks and opportunities

The TCFD recommendations require the disclosure of metrics and targets that will be used by the board to monitor climate-related risks and opportunities, and to measure performance against the targets set. Company secretaries should advise their boards to hold management accountable for climate-related performance by incorporating performance metrics into remuneration to incentivise the C-suite and executives. The role of the company secretary may also include:

- coordinating with management or the ESG function to suggest appropriate metrics and targets on key climate-related risks and opportunities for the board's consideration

- ensuring the board has discussed and approved relevant metrics and targets

- analysing metrics performance information and comparing against targets, and reporting to the board for regular monitoring and formulating measures to close any gaps, and

- ensuring disclosure of accurate metrics and targets information.

5. The company secretary's role in disclosure

Company secretaries have the primary responsibility for drafting the governance section of the company's annual and ESG reports. In the context of implementing the TCFD recommendations, as part of the ESG report, company secretaries should:

- coordinate and oversee the ESG/sustainability working group in collecting the relevant information required from different internal stakeholders for disclosure

- ensure the quality and accuracy of climate-related disclosure by obtaining independent assurance of the company's compliance with reporting principles and disclosure requirements

- ensure the disclosure of climate-related issues and that figures are appropriate and comply with TCFD recommendations requirements, and

- ensure that disclosures are reviewed and signed off by management and the board before distribution.

Conclusion

Regulators around the globe have been speeding up the pace of codifying aspects of the TCFD recommendations into relevant rules and regulations. Implementation of the TCFD recommendations has also been widely recognised by companies globally as a way to provide necessary climate-related information to stakeholders and address their concerns. These trends are expected to continue. Company secretaries, as governance professionals, are importantly positioned via their various roles to promote the importance of climate change risks and opportunities at the board level. They can play a key role in implementing the TCFD recommendations, and formulating strategic responses to climate change and ensuring the achievement of strategic goals for long-term viability. Depending on their readiness, boards may consider taking some small steps by implementing the TCFD recommendations in phases so as to get the ball rolling. Let's get started!

This article was first published in the January 2022 edition of CGj, the journal of the Hong Kong Chartered Governance Institute (www.hkcgi.org.hk), and published by Ninehills Media Ltd.

Subscribe to receive the latest BDO News and Insights

Please fill out the following form to access the download.